Industry insiders view embedded insurance as having the greatest growth potential in the distribution of personal lines insurance over the next five years, according to a GlobalData poll. Insurers who can navigate the evolving distribution landscape and adapt their distribution strategies will be best placed for success.

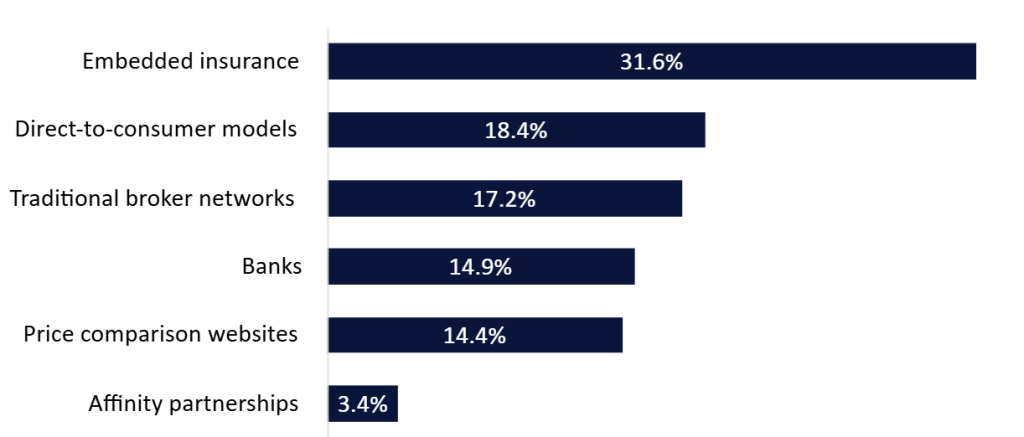

According to a poll conducted by GlobalData on Verdict Media sites in Q1 2025, which garnered over 170 responses from industry insiders, embedded insurance is the channel poised for the strongest growth in the distribution of personal lines insurance, as cited by 31.6% of respondents. The proportion of respondents betting for this channel is significantly higher than for direct-to-consumer models (18.4%) or traditional broking networks (17.2%), the other most prominent choices.

Go deeper with GlobalData

Which distribution channel will see the most growth in person lines insurance over the next five years? 2025

A key competitive advantage of embedded insurance is that policies are offered precisely when and where they are most relevant to customers, increasing the likelihood of a purchase. Embedded insurance involves integrating policies at the point of sale with a core product or service offered by a non-insurance business, and the broad nature of companies that can sell insurance magnifies growth opportunities. For instance, travel insurance can be offered during a flight booking, motor insurance when selling a car, or gadget insurance with electronic goods. In fact, this model allows insurers to reach customers who were otherwise not seeking to take out a policy.

From a customer’s point of view, embedded insurance offers convenience and time savings, allowing them to take out an insurance policy at the same time as they purchase another good or arrange a service. In addition, policies may also be priced more favorably, as embedding eliminates marketing costs.

While the concept of embedded insurance is not a new one, digital innovation and evolving consumer expectations have brought it to light. Digital platforms are gaining more and more importance in the embedded insurance model as consumers continue to shift away from brick-and-mortar stores towards online purchases, increasingly expecting frictionless experiences across industries.

Although the insurance distribution landscape is becoming more diverse and digitally driven, insurers must still ensure presence across all distribution channels to cater for the preferences or needs of individual customers. Insurers who can successfully navigate this evolving distribution landscape at a time when consumer preferences are changing will be best placed for success. This will involve adapting their distribution strategies and embracing digital innovation to ensure they remain relevant.