Almost half (48.2%) of firms in the UK have mandated working from home during the COVID-19 pandemic, according to Office for National Statistics data. During the Covid-19 lockdown, home insurance policies will fully compensate a home-working claimant, but policyholders will have to amend their cover once the lockdown is lifted.

Because of the government-mandated lockdown, there is a record number of individuals working from home, and it is expected that many will continue to do so after the crisis subsides. Working from home offers employees a greater work-life balance and can help businesses cut down on overhead costs.

Go deeper with GlobalData

Covid-19 and home insurance

While home insurance cover will not be affected during the lockdown, policyholders will need to notify their insurers if they plan to continue working from home regularly once the lockdown is lifted. Working from home could increase the risk at a property due to expensive equipment being stored there, as could regular visitors to the property due to increased theft or liability risk.

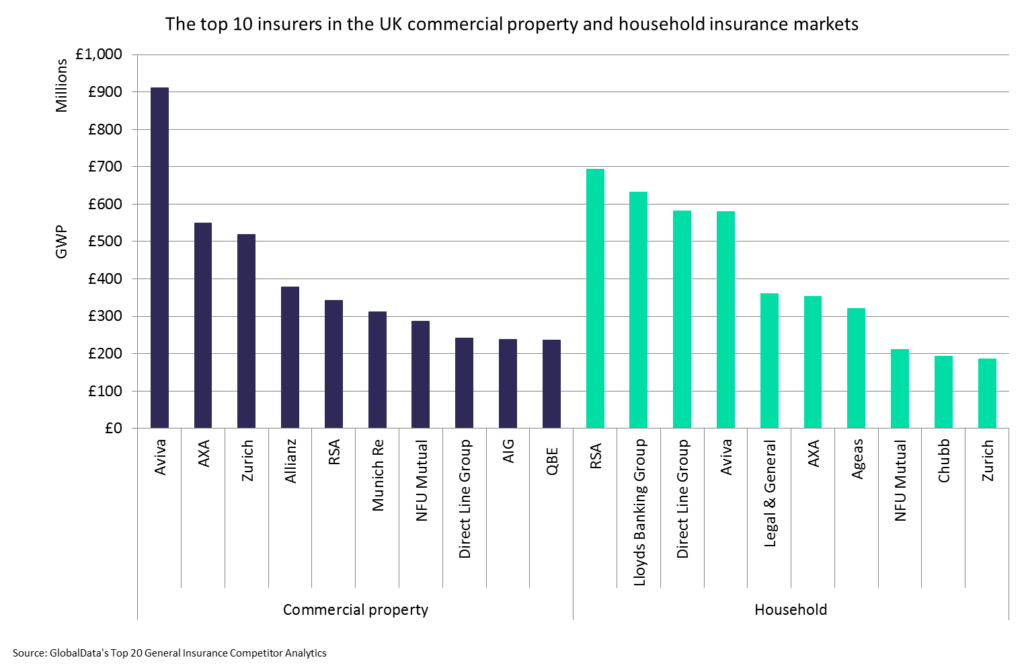

On the other hand, businesses will not need as much office space and will have fewer contents on their premises, reducing the premiums on commercial property policies. This shifts risk away from commercial property towards home insurance, and premiums generated in the two business lines will need to be adjusted accordingly.

Aviva, AXA, Zurich, RSA, and NFU Mutual all have strong market positions in the UK in both the household and commercial property markets, which puts them in a strong position to capitalise on the shift in premiums. Lloyds Banking Group is the second largest underwriter of household insurance and stands to benefit the most from a shift in premiums away from the commercial property sector. On the other hand, Allianz’s stronger position in commercial property insurance compared to household insurance may result in it taking more of a hit.

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalData