The insurance industry continues to be a hotbed of innovation, with activity driven by growing demand for digitalisation and personalisation. With growing importance of technologies such as telematics, machine learning, big data, deep learning, and data science, insurers are overcoming demographic challenges, low penetration rates, cybercrimes and fraudulent claims. In the last three years alone, there have been over 11,000 patents filed and granted in the insurance industry, according to GlobalData’s report on Artificial intelligence in Insurance: Dynamic premium pricing. Buy the report here.

Smarter leaders trust GlobalData

However, not all innovations are equal and nor do they follow a constant upward trend. Instead, their evolution takes the form of an S-shaped curve that reflects their typical lifecycle from early emergence to accelerating adoption, before finally stabilising and reaching maturity.

Identifying where a particular innovation is on this journey, especially those that are in the emerging and accelerating stages, is essential for understanding their current level of adoption and the likely future trajectory and impact they will have.

90 innovations will shape the insurance industry

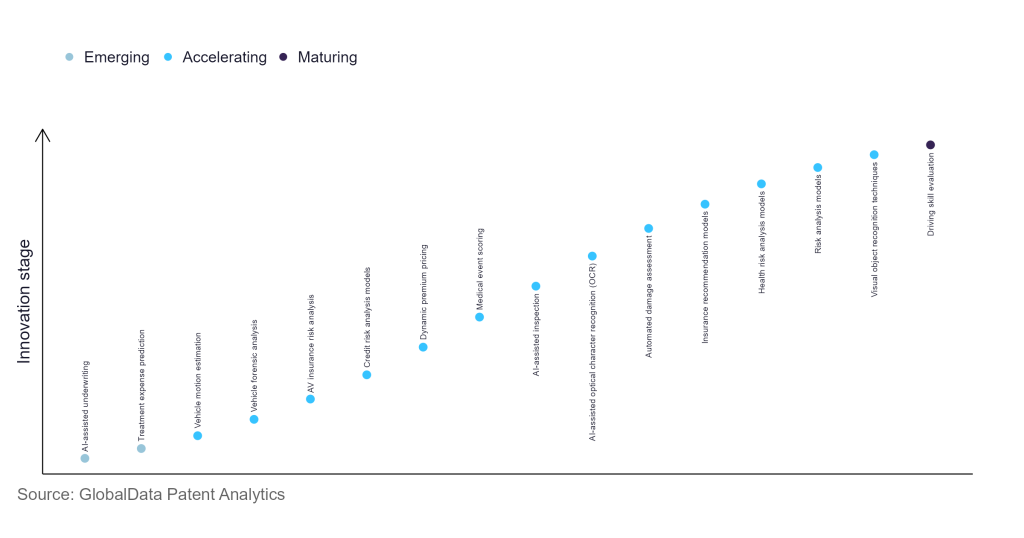

According to GlobalData’s Technology Foresights, which plots the S-curve for the insurance industry using innovation intensity models built on over 65,000 patents, there are 90 innovation areas that will shape the future of the industry.

Within the emerging innovation stage, AI-assisted underwriting and treatment expense prediction are disruptive technologies that are in the early stages of application and should be tracked closely. Vehicle motion estimation, vehicle forensic analysis, and AV insurance risk analysis are some of the accelerating innovation areas, where adoption has been steadily increasing. Among maturing innovation areas is driving skill evaluation, which is now well established in the industry.

Innovation S-curve for artificial intelligence in the insurance industry

Dynamic premium pricing is a key innovation area in Artificial Intelligence

Dynamic pricing allows insurers to update policy pricing based on real-time market changes and consumer expectations. With AI capabilities, insurers can customise prices automatically, based on consumer risk profile and coverage needs. As a result, lower-risk customers can be offered low-cost policies, while high-risk policyholders will have a higher premium pricing. For instance, AI dynamic premium pricing for motor insurance would calculate customer risk through factors such as usage, driver history and risk-averse behaviour, road conditions and weather.

GlobalData’s analysis also uncovers the companies at the forefront of each innovation area and assesses the potential reach and impact of their patenting activity across different applications and geographies. According to GlobalData, there are 170+ companies, spanning technology vendors, established insurance companies, and up-and-coming start-ups engaged in the development and application of dynamic premium pricing.

Key players in dynamic premium pricing – a disruptive innovation in the insurance industry

‘Application diversity’ measures the number of different applications identified for each relevant patent and broadly splits companies into either ‘niche’ or ‘diversified’ innovators.

‘Geographic reach’ refers to the number of different countries each relevant patent is registered in and reflects the breadth of geographic application intended, ranging from ‘global’ to ‘local’.

Patent volumes related to dynamic premium pricing

Source: GlobalData Patent Analytics

State Farm Mutual Automobile Insurance is one of the leading patent filers in use of AI in dynamic premium pricing. The company’s computer-implemented method offers an insured customer incentives for receiving sensor data showing risk-reducing and risk-increasing behaviour patterns during the policy term. In-vehicle sensors or other devices collect information about the vehicle and its use and send it to a back-end system for analysis. Based on this analysis, the back-end system may take one or more actions defined by a set of rules to create an incentive or disincentive for the customer based on the behaviour. For example, the system may modify the customer's insurance policy data, send an e-mail, letter, gift card, coupon, points, or other communication to the customer. Some other key patent filers include SoftBank Group, Ping An Insurance, The Allstate, and PayPal.

In terms of application diversity, INRIX leads the pack, with Alphabet and Flex in the second and third positions, respectively. By means of geographic reach, Catch Media holds the top position, followed by Swiss Re and Warrantee.

To further understand the key themes and technologies disrupting the insurance industry, access GlobalData’s latest thematic research report on Insurance.

Data Insights

From

![]()

The gold standard of business intelligence.

Blending expert knowledge with cutting-edge technology, GlobalData’s unrivalled proprietary data will enable you to decode what’s happening in your market. You can make better informed decisions and gain a future-proof advantage over your competitors.

GlobalData, the leading provider of industry intelligence, provided the underlying data, research, and analysis used to produce this article.

GlobalData’s Patent Analytics tracks patent filings and grants from official offices around the world. Textual analysis and official patent classifications are used to group patents into key thematic areas and link them to specific companies across the world’s largest industries.